(QRTEA) Qurate Retail: A Turnaround Story

Mon Dec 04 2023/3 minute read

I’ll preface this post by saying that this is one of the more complex businesses that I’ve got involved with. The debt structure of this company is complex and there are significant risks involved. I’ll suggest to size the position accordingly.

Qurate Retail ($352.95M market-cap) is the holding company for QVC, HSN, Ballard Designs, Frontgate, Garnet Hill, and Grandin Road - all dedicated to providing consumer products through televised shopping and via their online apps. Qurate Retail Group is the largest player in video commerce, which includes video-driven shopping across linear TV, ecommerce sites, digital streaming, and social platforms. It’s also part of John Malone’s larger Liberty Media empire.

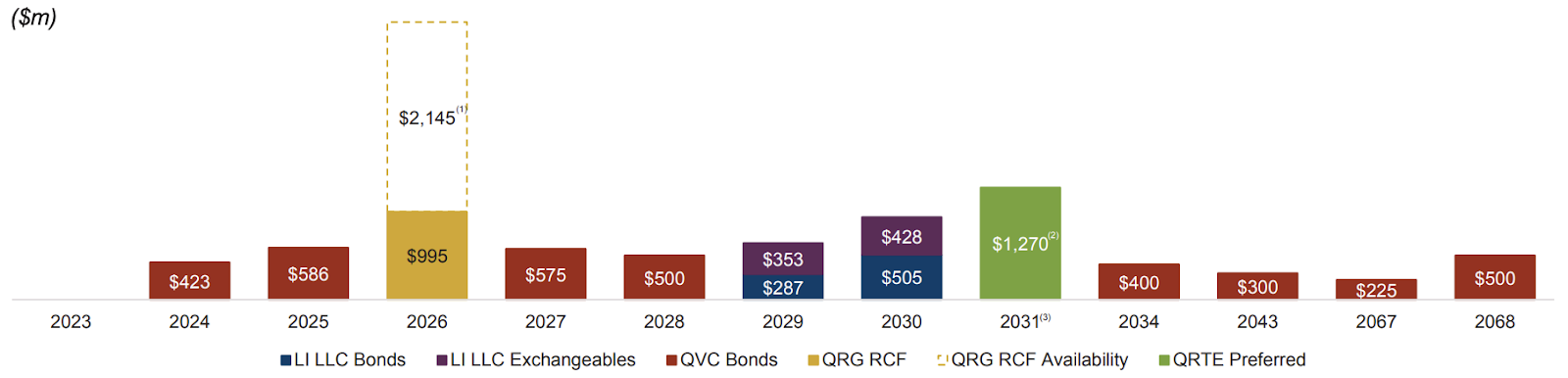

Qurate, however, is saddled in debt. The series A common stock has been decimated, losing 94% of its value from the covid highs of 2021. Qurate also has a rather complex capital structure; it has $590M of common equity (QRTEA & QRTEB), $1.27B of preferred stock yielding 8% (QRTEP), and another $3.51B of bonds. Here’s the maturity schedule on the debt/RCF:

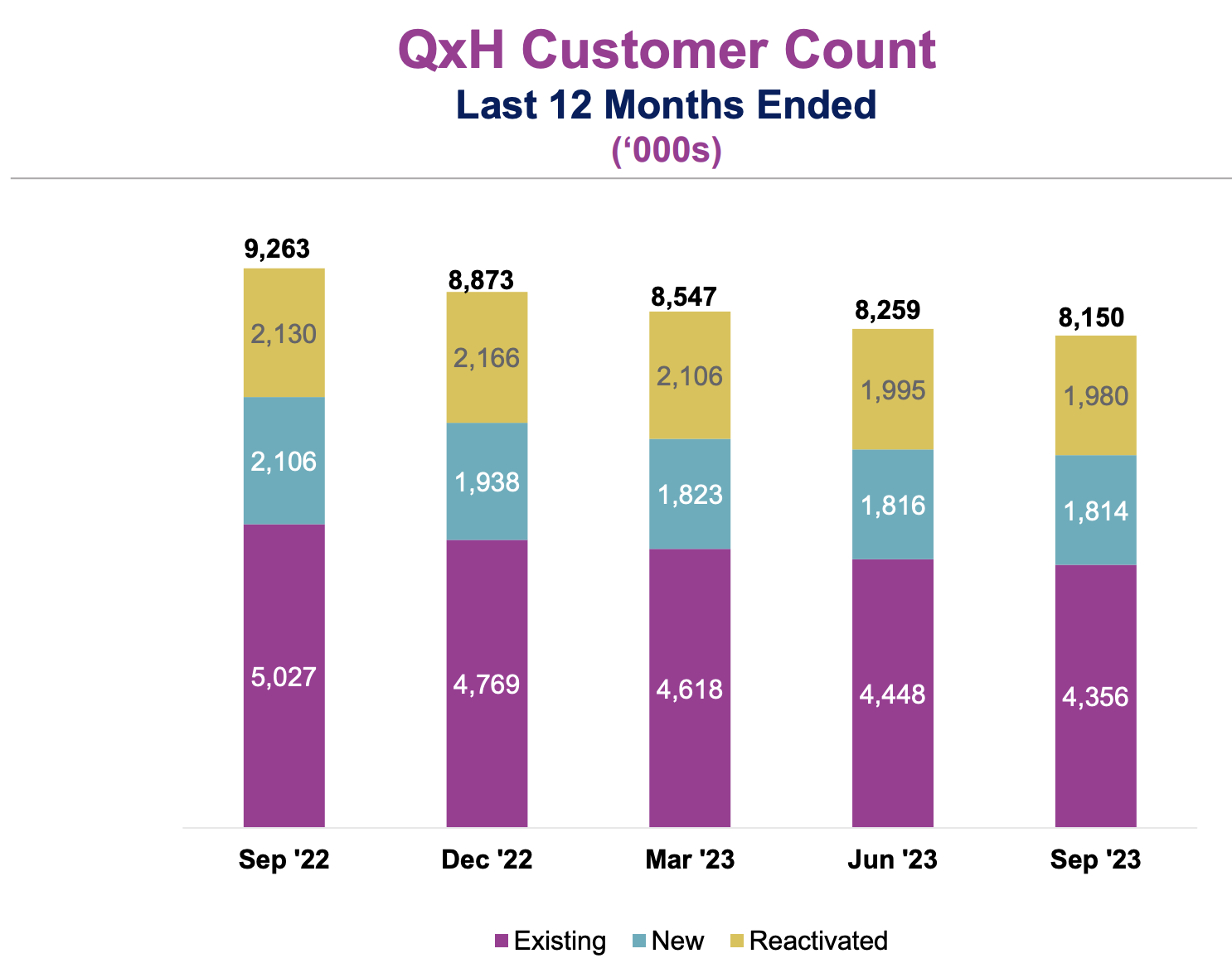

The bonds also trade for a significant discount to face value, signaling strong bankruptcy fears priced in. In addition, a major concern is Qurate’s dropping user count. From the latest earnings report:

Management cited cord cutting as a big reason for this drop, since users are spending more time outdoors post-covid resulting in drop of cable TV usage. To add to the misery, a fire in December 2021 destroyed the company's second largest logistics center in Rocky Mountain, NC, from which 25-30% of customer orders were shipped. All in all, Qurate finds itself in a grim situation. Customers are leaving, the company is facing one round of layoffs after another, and debt is mounting.

In 2022, to address these concerns, the new CEO David Rawlinson launched a three year growth plan called Project Athens. The five-point plan includes actions intended to strengthen customer relationships, improve execution, reduce costs, optimize the brand portfolio, and grow faster in streaming. Management’s projection is to reach $300M-$500M free cash flow by 2025 and the operating history of the company definitely suggests that it could be possible.

The good news is that since then, the management has indeed executed on many of these said points and the return-to-growth plan looks currently on track. Among other things, as revealed from their latest earnings–the company raised liquidity by closing sale of some real estate and leasebacks for UK/Germany warehouses, divested the money losing segment Zulily to simplify portfolio and improve liquidity, finalize $660M in insurance proceeds from Rocky Mountain fire (of which $280M received YTD), reduced $741M YTD in debt, repurchased $177m 2024 QVC notes and $15m 2025 QVC Notes at a discount.

With shares trading at such depressed prices, a buyback could be extremely accretive but the management has committed to using FCF to reduce debt which has the potential to magnify returns from current valuation.

In the plausible scenario of the recovery plan staying the course, Qurate should continue to reduce debt covenants, and with over $4B of bonds and preferred not due until 2030 or later, Qurate can continue buying back more debt at discounts, refinance near term maturities, and get back to stock repurchases with any residual cash. Qurate currently trades for 4.5 EV/EBITDA, which is far lower than other retailers like Walmart, TJMaxx etc. which hover in the lower teens. Considering a $5B EV on top of a ~$500 FCF, if Project Athens continues as planned, this could be a potential multibagger.

The downside here is more obvious, that Qurate yields under the mountain of debt, files for bankruptcy with the common and preferred holders likely left with nothing. The bonds, however, could see some recovery based on the proceeds post-bankruptcy.

Disclosure: I own shares of QRTEA